Every cyber-insurance renewal still runs on a document that was obsolete the day it was signed: the self-attested application. Your broker sends a questionnaire, a security lead answers forty to two hundred questions from memory and a few screenshots, a senior officer signs a warranty, and an underwriter prices a year of coverage off that snapshot. The structural problem is not dishonesty. It is that a yes/no questionnaire compresses a complex, drifting control environment into binary claims with no evidence attached, and underwriters know it. So they price for the ambiguity. The premium you pay includes a margin for everything they cannot verify, and that margin is the money left on the table.

Why a questionnaire leaves money on the table

Consider how a single line on the application actually behaves in the wild. 'Do you enforce multi-factor authentication on all remote access and privileged accounts?' The honest answer for most organizations is 'mostly.' MFA is on for the VPN and the email tenant, but there are three service accounts excluded for a legacy integration, a contractor population on a separate identity provider, and a break-glass admin account that nobody wants to touch. On the questionnaire that becomes a 'yes,' because 'mostly' has no box. The underwriter cannot see the exclusions, so they assume the worst case for accounts they cannot observe and price accordingly. You get penalized for the gap and for the opacity at the same time.

The asymmetry runs deeper than any one control. The underwriter is being asked to take a financial position on your loss distribution, but the only inputs they receive are categorical self-attestations and industry base rates. They have rich actuarial data on what claims cost across a book of business; they have almost nothing trustworthy about where your specific organization sits inside that distribution. In the absence of organization-specific evidence, they default to the cohort. If your controls are genuinely better than your peers', the questionnaire gives you no mechanism to prove it, so you subsidize the weaker firms in your rate class. The whole point of bringing verified evidence is to move yourself off the cohort curve and onto your own.

An underwriter-reviewable package

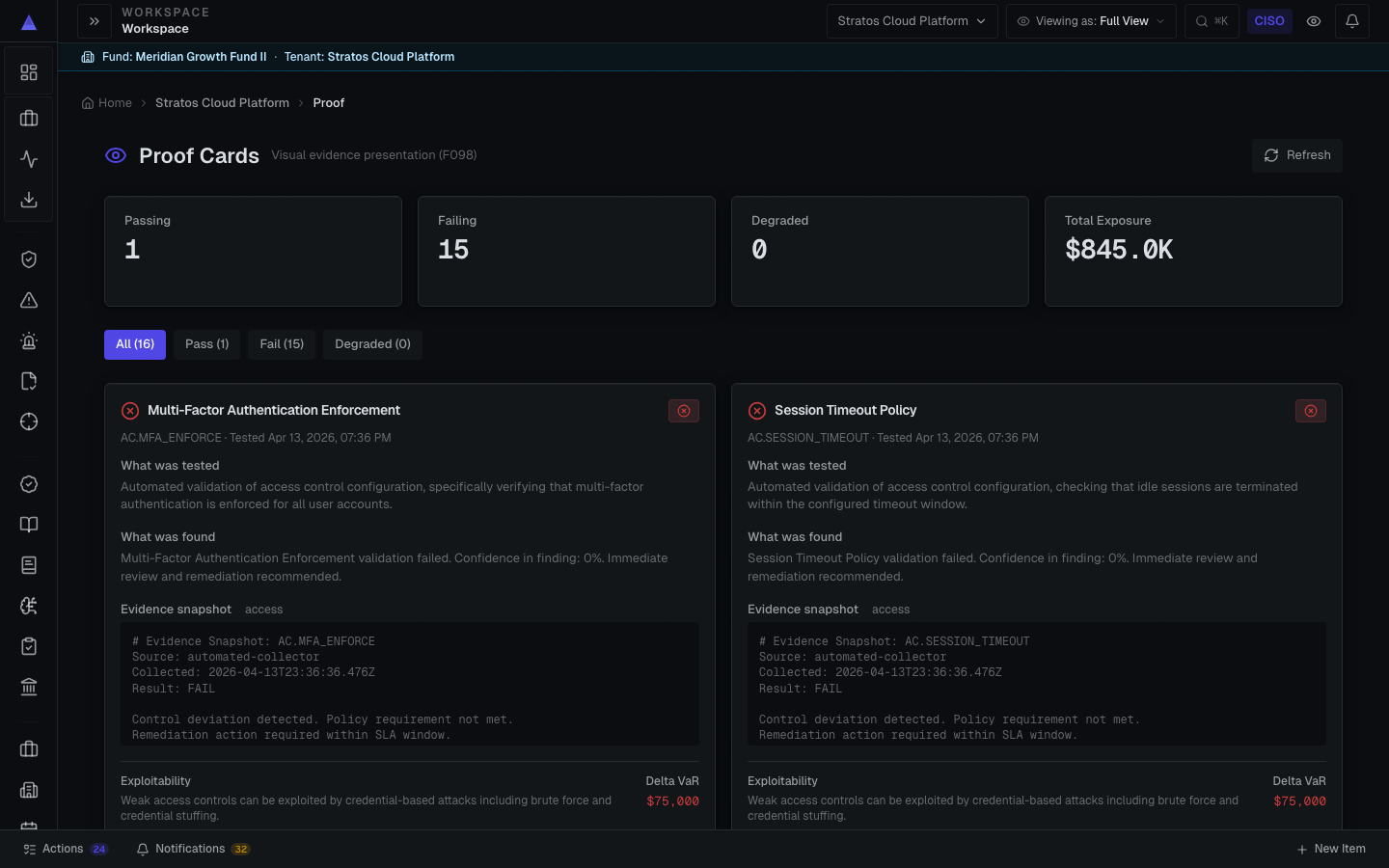

An underwriter-reviewable evidence package is the alternative, and it has two halves that do different jobs. The first half is verified control state: not 'we have MFA' but a current, sourced statement of which identities are covered, which are excluded and why, when that was last observed, and where the observation came from. The second half is a quantified exposure range: the financial loss your remaining control gaps could plausibly produce, expressed as a distribution rather than a single number. The first half tells the underwriter what is actually true today. The second half tells them what it is worth in dollars if it fails. Together they replace 'trust our checkbox' with 'inspect our evidence.'

Verified control state means the claim and the proof travel together. Instead of asserting endpoint coverage, you show the count of managed endpoints against the count of known assets, the percentage reporting to the EDR in the last twenty-four hours, and the date of the reading. Instead of asserting that backups are immutable and tested, you show the last successful restore test and the retention configuration as read from the backup system itself. Valty is built to assemble exactly this kind of package by reading from the tools you already run, the scanners, cloud accounts, identity providers, and GRC systems, rather than asking a human to re-key their status into a form. It does not replace those tools; it reconciles what they report into a single reviewable statement of control state with the source and timestamp attached to each line.

The quantified exposure range

The quantified exposure half is where senior buyers should be most careful, because this is where vendors most often overclaim. Valty's approach is FAIR-aligned Monte Carlo: it models loss event frequency and loss magnitude for your specific gaps, runs the simulation thousands of times, and reports a range, typically a P10, a base case, and a P90, rather than a single confident figure. A range is the honest representation because the underlying inputs are uncertain, and showing the spread is more credible to a skeptical reader than a precise-looking point estimate. Every figure carries its method, its confidence, and its source so the recipient can interrogate the assumptions instead of being asked to swallow a conclusion.

It is worth stating plainly what this is and is not. Valty is not an insurer, not a broker, and not a rating agency. The exposure figures are decision-support estimates to structure a negotiation, not actuarial prices, not a guarantee of loss, and not investment or legal advice. The underwriter still owns the pricing decision and will apply their own models, their loss data, and their judgment. What the evidence package changes is the quality of the inputs they price against. You are not trying to do the underwriter's job; you are trying to remove the uncertainty premium they would otherwise charge for not being able to see clearly.

The negotiation changes character

When you bring this package to the table, the negotiation itself changes character. A questionnaire renewal is a one-way transfer of unverified claims followed by a take-it-or-leave-it quote. An evidence-backed renewal is a conversation about specific, inspectable facts. The underwriter can ask why three service accounts are excluded from MFA and you can show the compensating control and the remediation date. They can challenge a frequency assumption in the loss model and you can show the input it came from. Specifics invite negotiation; vagueness invites a margin. The firms that win better terms are usually not the ones with flawless controls, they are the ones who make their actual control state legible enough to argue about.

Sequencing remediation for renewal leverage

The same evidence base also reframes how you spend remediation dollars before the renewal, which is often where the largest savings hide. Because the exposure model ranks gaps by the financial loss each one drives, you can see which fixes actually move the number an underwriter cares about and which are hygiene that will not change a quote. Closing a gap that carries a wide, high-magnitude loss tail, and being able to show it was closed with a dated, sourced reading, is the kind of change that justifies a premium reduction or a higher sublimit. Closing ten low-impact findings may improve your security posture but will not, on its own, give the underwriter anything to reprice. Knowing the difference lets you sequence work for both security and renewal leverage.

The snapshot versus the stream

Then there is the matter of the snapshot versus the stream, which is the deepest structural flaw in the annual-application model. A questionnaire is true, at best, on the day it is signed, and control state drifts continuously: a new cloud account is stood up without logging, an acquired subsidiary arrives with an unknown identity estate, an EDR agent silently stops reporting on a tranche of laptops. None of that is visible at the next renewal because the next data point is twelve months away. The warranty you signed becomes progressively less accurate the moment after you sign it, and in a claim that drift can become the basis for a coverage dispute.

Continuous evidence attacks that flaw directly. When control state is read on an ongoing basis rather than reconstructed once a year, you can hand the underwriter a current package at renewal instead of a stale recollection, and you can detect and document drift while there is still time to fix it. The practical defensive value is significant: at claim time, the question of whether a control was actually in force on the date of the incident is answered by dated, sourced readings rather than by a year-old checkbox and a dispute over what 'all privileged accounts' meant. A continuous record is both a better negotiating asset and a better record to have if you ever need to substantiate that your representations were accurate when made.

The limits, held in view

None of this eliminates the genuine limits, and a credible buyer should hold them in view. The evidence package is only as good as the systems it reads from; if your asset inventory is incomplete, the coverage percentages computed against it are optimistic, and you should say so rather than let a clean-looking number imply completeness. The loss model depends on assumptions that reasonable people will dispute, which is exactly why the range and its sources are visible. And an underwriter is under no obligation to reward better evidence with better terms; some will, some will price the same way regardless. The package improves your position; it does not control the counterparty's decision.

The honest summary for a CFO or CISO is this. You are almost certainly overpaying some amount of uncertainty premium today because your renewal runs on self-reported claims an underwriter cannot verify, and you have no instrument to prove you are better than your rate class. An underwriter-reviewable package, verified control state plus a quantified, FAIR-aligned exposure range with methods and sources exposed, gives you that instrument and turns a take-it-or-leave-it quote into a negotiation over inspectable facts. Valty's role is to assemble that package from the tools you already run and keep it current, as decision support, not as a price and not as a promise. The savings, if they come, come from making your real risk legible enough that nobody has to guess.